The results of our study have shown that creditworthiness is a complex multifaceted characteristic of the enterprise-borrower, which includes many criteria that have important scientific and practical value. From a practical point of view, the knowledge of these parameters, the mechanism of their influence on creditworthiness is the basis for the development of a scientifically based methodology for the credit assessment of the client’s enterprise in the bank.

The study of banks shows a variety of factors that may result the nonpayment of loans, or, conversely, ensure their timely return, form the contents of the assessment by the bank of the creditworthiness of the borrower.

Generalizing the criteria of creditworthiness allocated by domestic and foreign authors, we can say that, in fact, when analyzing the creditworthiness of banks should assess the formal and informal indicators of creditworthiness of the borrower, and through them to assess the borrower’s ability to meet its obligations in time and willingness of their execution. The first question gives the answer assessment of formal parameters:

— probability of bankruptcy;

— the potential of enterprise (manufacturing-industrial and financial);

on the second question – the assessment of informal indicators:

— legal security of the loan;

— professional culture of the borrower.

Usually the formal parameters are defined through analysis of financial and economic activity of the enterprise. This analysis includes the definition of performance indicators, methods of their measurement and characteristics of these indicators according to certain principles, evaluation of deviations from the standard, accepted values [1]. In the study of the system of analytical indicators mainly use the deductive method, involving the transition from the general to the specific.

In modern conditions of business it becomes obvious that the heads of economic entities to survive and preserve long-term competitiveness must constantly adjust their activities to reflect the needs of the environment. The new business environment assumes constant willingness to change.

The external environment of enterprise is changing faster and more predictable. While every change brings not only threats, but also new opportunities it should achieve future business success. The head of the enterprise must have the ability to properly and timely to transform the structure of its business, routinely adequate strategic and operational changes.

The lack of strategic concepts for enterprise behavior in the market leads to the dissipation of forces and means total lack of control of material and financial resources. Therefore, there is a real need for the creation and implementation of mechanisms to control various processes of the company, including creditworthiness, allowing perceive these changes, to recognize them and provide appropriate adaptation of the production and commercial activities of enterprises to market conditions.

Any company can be considered as an economic system, which as basic concepts use concepts such as «economic mechanism», «organizational-economic mechanism, «financial mechanism», «the market mechanism», «structure», «economic interests,» «strategic management», etc.

Became the classic definition of organizational-economic mechanism as a complex and interdependent set of elements of organizational, economic, and sometimes technologically interconnected subsystems of lower level (figure 1). The hallmark of such an enterprise as a system is the availability of real (explicit, measurable) relationships of certain economic processes that can be to classified and clustered. Detected at the same time dependence (influence) stipulates the need to formulate the concept of organizational-economic mechanism. In the literature there is no clear understanding of both the organizational-economic mechanism and its essence.

In the Economic dictionary the term «mechanism» is defined as «a sequence of states, processes that determine some action, phenomenon, or system, the device that determines the order of some activity». The economic mechanism is defined as «a set of economic structures, institutions, forms and methods of management. Is the linkage and coordination of public, group and private interests, ensures the functioning and development of the national economy.» [2].

The authors of the Modern economic vocabulary called this category as «a set of organizational structures, specific forms and methods of management and legal standards, which are implemented through operating in a specific economic laws, the process of reproduction». So, A. Kullmann claims that the «economic mechanism is determined either by the nature of the original phenomenon, or the end result of a series of phenomena,» and clarifies that «the constituent elements of the mechanism is always simultaneously act as the source phenomenon, and result phenomena, and the whole process that occurs in the interval between them» [3]. In other words, any organizational-economic mechanism there is a certain set or sequence of economic phenomena [4].

In table 1 we see the stages and characteristics stages of the organizational-economic mechanism of implementation of credit operations, including stages from loan application consideration to repayment of the loan.

In our study, more detail will be considered the stage and the creditworthiness rating of the borrower from the point of view of both domestic and external factors to determine on the basis of analysis of the integral potential of a company’s creditworthiness.

Based on the definitions above we propose to consider organizational and economic mechanism of management of creditworthiness of the enterprise as a series of actions aimed at ensuring the interaction of economic and organizational elements, including the identification and evaluation of factors affecting the creditworthiness of the enterprise, determining the potential creditworthiness of the enterprise and management decisions for improving it.

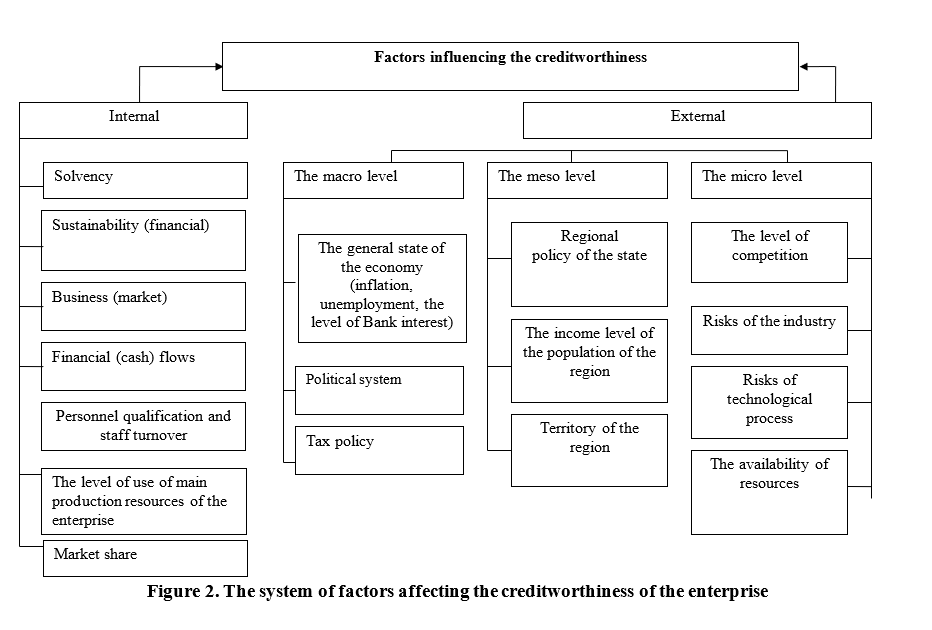

Fig.2 shows the system factors affecting organizational-economic mechanism of management of creditworthiness of the enterprise depends on how the restoration of creditworthiness of loss-making enterprises, and the risk of insolvency of the creditworthy businesses.

Table 1

Stages of organizational-economic mechanism of implementation of credit operations

| № | Stage | Characteristics of the stage | |

| 1 | 2 | 3 | |

| 1 | Loan application | Involves performing the following procedures: — pre-qualification of a potential borrower; — gathering the necessary information and documents according to the approved list; — check the truthfulness of information and documents; — identification and analysis of criminal risks; — identification and analysis of legal risks; — analysis of information and documents, evaluation of credit risks | |

| 2 | Consideration of possible forms of security for the repayment of the loan | Define the form of collateral for a loan (collateral, pledge, Bank guarantee, surety, security deposit), carrying out the assessment of collateral. When deciding on the conclusion of the contract of pledge/mortgage, take into account the presence of the mortgagor of the documents confirming the ownership right to the collateral/mortgage. Written consent of the owner of the immovable property pledge/mortgage, when the mortgagor is given the right of full economic management, operational management, rent. | |

| 3 | The determination of creditworthiness | The assessment shall be: the market position of the borrower; the financial condition of the borrower and its creditworthiness, the analysis of the structure of the balance sheet items; the quality of assets, receivables and payables; transaction financing; scheme and terms of payments to contractors on the basis of the analysis of contract documents; marketing policy of the enterprise; sources of repayment of the obligations to the Bank; liquidity and sufficiency of collateral. | |

| 4 | A decision on a credit application | The average period of employment with a specific credit application is 7 – 10 days from the date of granting by the borrower of a full package of documents. Credit Management/Department of resource management and Risk Management are written opinions (reasoned judgment) on the ability or inability of the loan. The application is reviewed and accepted (rejected) on the credit Committee of the Bank. |

| 5 | The conclusion of the credit agreement | Execution and monitoring of contract performance by the Credit Management Control / Accounting Management and correspondent relations |

| 6. | Delivery of credits | Provision of funds to borrower (the credit line). |

| 7. | Execution and maintenance of credit files of the borrower | Each borrower is formed and maintained credit files, in accordance with applicable regulations. In credit affairs (dossier) is represented by the contractual framework of the financed transactions, copies of contracts, documents for loan security, financial statements of borrowers and guarantors, data on borrowers from other banks, the analysis of the documents of the borrowers, professional judgment risk assessment. |

| 8. | Maintenance and monitoring of credit agreements and loan portfolio | Continuous monitoring of credit agreements to ensure proper performance by the borrower of its obligation to repay the principal amount, interest on the loan and refund to the Bank all other costs provided for enclosed operation: the control of target use of loans; analysis of cash flow on accounts of the borrower; quarterly analysis of the financial model status of the borrower; an analysis of the information about the economic, sectoral and political factors that may affect the borrower’s ability to repay the loan; timely identification of signs of problem loans; monitoring other relevant factors. The transmission of information to the Bank credit history. |

| 9. | Work with the problem credit | Ensuring full repayment of funds provided by the Bank to the Borrowers. It is necessary to identify of problem loans at an early stage. |

| 10. | Repayment of the loan | Is carried out from funds received by the borrower in its financial and economic (work) activities in accordance with the terms of the loan agreements. |

Библиографический список

1. Zernova L.E., Sagan S.I. Methodical approach to the definition of a company's creditworthiness. News of higher educational institutions. Technology of textile industry. 2010. No. 3. pp. 3-6.2. Zernova L.E., Titarenko K.A. THE METHODOLOGICAL APPROACHES TO DEFINITION OF CREDITWORTHINESS OF ENTERPRISE. Materials of XI international scientific-practical conference, SIC "Academic". 2017. p. 176-179.

3. Zernova L.E., Guseva D.S. EVALUATION OF CREDIT CUSTOMERS OF A COMMERCIAL BANK AS A FACTOR IN REDUCING CREDIT RISK Proceedings of the VI International youth scientific conference: Youth and XXI century - 2016 . 2016. pp. 173-176.

4. Zernova L.E., Guseva D.S. THE PROCEDURE OF ASSESSING THE CREDITWORTHINESS OF CUSTOMERS AS AN INTEGRAL PART OF THE BANK'S CREDIT POLICY. Collection of articles of International scientific-practical conference: NEW INFORMATION TECHNOLOGIES IN SCIENCE . 2016. pp. 39-42.