Introduction

Since there is heightened competition for rare natural resources, strategic metals have become even more vital to national security and economic stability of States. Strategic metals are required for the manufacture of sophisticated high-technology goods, i.e., renewable energy appliances, defense equipment, batteries, and electronics. The USA, as one of the world’s economic giants, is particularly vulnerable to the need for sustainable access to these metals since the majority of the demand comes through imports. Geopolitics, rising protectionism, and exposure of international supply chains enhance the risk of supply disruptions, which would adversely impact key industries. In such cases, the effort of evolving a long-term strategy with a focus on reducing dependency on external sources is achieved.

Public and private initiatives towards the development of home production, the stimulation of refining, and improving international cooperation are becoming the national economic agenda. The aim of this study is to examine the USA’s economic and geopolitical policy initiatives introduced in an attempt to diversify the supply of strategic metals with an emphasis on systemic policies directed at increasing the independence and sustainability of the resource supply.

Main part. Current position of the USA in the global supply chain of strategic metals

The USA current role within the global supply chain of the strategic metals is that of a high import dependency within an environment of extensive but untapped domestic supplies. Foreign market concentration of the USA industry over the decades has contributed to building structural vulnerabilities in supply chains. This issue is most critical in the rare earths, cobalt, lithium and graphite sector that is key to battery, weapons system and renewable energy equipment production.

In the present structure of the world market, the USA plays the position of primarily an import-dependent economy in the strategic metals industry. According to the U.S. Geological Survey, the country is fully dependent on imports of more than 15 types of minerals, including rare earths, beryllium and niobium. The major suppliers are States with unstable political situations or competing foreign policy agendas, which further increases the risks. In particular, a large proportion of rare earth metals is being produced in China, which, according to various estimates, accounts for more than 80% of the world’s production and processing in the sector (Table 1).

Table 1

USA mineral-related economic trends [1]

| Indicator | 2020 | 2021 | 2022 | 2023 | 2024 |

| GDP (billion USD) | 21,354 | 23,681 | 26,007 | 27,721 | 29,179 |

| Industrial production index (2017 = 100) | |||||

| All industry | 95 | 99 | 103 | 103 | 100 |

| Manufacturing: | |||||

| Nonmetallic mineral products | 97 | 101 | 107 | 106 | 100 |

| Primary metals | 87 | 96 | 95 | 95 | 94 |

| Iron and steel | 87 | 102 | 96 | 97 | 93 |

| Aluminum | 92 | 97 | 96 | 91 | 94 |

| Nonferrous metals | 92 | 95 | 105 | 108 | 110 |

| Chemicals | 95 | 100 | 102 | 104 | 110 |

| Mining | 103 | 106 | 114 | 120 | 120 |

| Metals | 95 | 92 | 86 | 80 | 80 |

| Capacity utilization (%) | |||||

| Total industry | 73 | 78 | 81 | 79 | 78 |

| Mining | 72 | 82 | 90 | 90 | 89 |

| Metals | 66 | 62 | 56 | 53 | 53 |

| Nonmetallic mineral products | 84 | 87 | 90 | 89 | 85 |

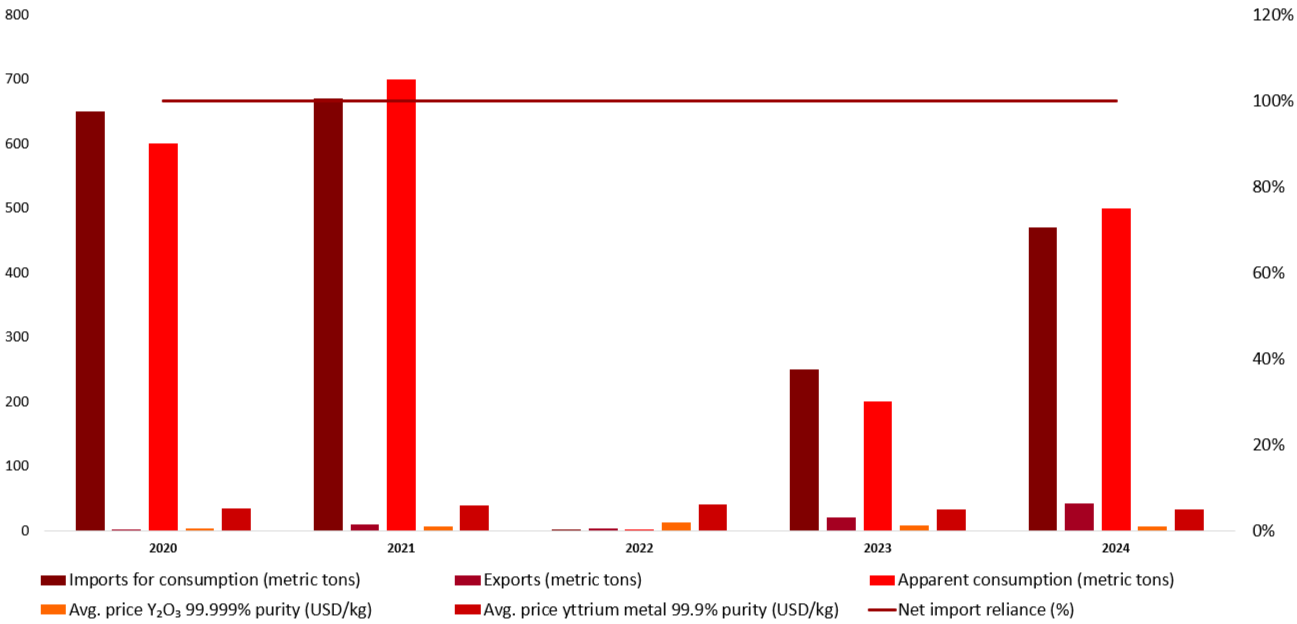

Statistics reveal that due to overall GDP growth and operation of mining, steel sector capacity has remained low over the past five years. The analogy of strong demand for the nation versus slow indigenous processing capacity captures systemic weakness of the USA mineral supply system. Still, special attention should be paid to the assets of USA domestic production long relegated to the fringes of the national resource planning. The most – familiar example is the Mountain Pass deposit in California, which in the 1990s was the major source of rare earth metals in the USA, but later turned out to be non – competitive compared to Chinese producers (fig. 1).

Figure 1. USA yttrium supply and trade data (2020–2024) [2]

Only in recent years, with the intensification of sanctions policy and trade wars, has investment for development and processing in this plant been resumed. Still, despite the acceleration, domestic production for most metals remains insufficient to meet demand in high-tech industries.

Thus, the current position of the USA in the global supply chain of strategic metals is marked by a combination of high import dependence and low elaboration of its own raw materials base. This represents a vital vulnerability under conditions of geopolitical transition and compels the task of resource security to emerge as a priority thrust area of state policy.

Geopolitical initiatives to reduce dependence on imports

As a response to increasing geo-economic pressures, the USA is proactively moving in foreign policy direction towards reducing strategic metals import reliance. These actions are all part of the overall reorganization of global supply chains and strengthening the nation against increasing competition for resources. The geopolitical aspect is emerging as a key consideration in creating a sustainable model of access to strategic materials, especially in the context of the strained relationship with China and uncertainty in a number of supplier countries.

One of the significant steps was setting up global alliances on mineral security issues. The USA spearheaded the creation of the Minerals Security Partnership (MSP), dedicated to establishing clean and transparent supplies of strategic metals with G7 partners as well as Indo-Pacific nations. The objective of such pacts is not just to diversify the sources of raw materials, but also to introduce common standards of environmental and social responsibility in the processing and extraction industry. The MSP is aimed at nations like Canada, Australia, and South Korea, which are significant allies of the USA with huge resources and stable political systems [3].

At the same time, the USA is actively including the «mineral diplomacy» component in bilateral free trade and strategic partnership agreements. An example is the development of economic cooperation with Canada in the lithium and nickel fields, and with Australia in the field of rare earth metals. These agreements cover not only supply guarantees, but also joint investment in logistics and processing infrastructure. In addition, the White House-supported Build Back Better World Initiative plans to invest in the development of the mining industry in low- and middle-income countries, which will allow the USA to expand access to new sources of raw materials [4].

Thus, USA geopolitical efforts demonstrate a strategic trend in reducing resource dependence through the strengthening of foreign alliances, promotion of common standards, and the formulation of alternative supply routes. They are ever more an industrial and national security policy and strategy for the long term.

Geo-economic tools and foreign policy positioning of the USA

Geo-economic tools are the essence of the USA strategic arsenal of obtaining sustainable access to strategic metals. This economic policy change follows the change from the classic liberal doctrine to more state involvement in the regulation of resource supply and foreign economic relations. The USA hopes not only to diversify supply but also to create a new geo-economic area where strategic materials become a matter of political regulation and an instrument of global power.

The export control and investment restraint policy are probably the most significant geo-economic coercion tool. Using tools such as the International Emergency Economic Powers Act (IEEPA) and the Committee on Foreign Investment in the USA (CFIUS), the government constrains strategic transactions that can undermine national security. These measures have been particularly consolidated in the context of growing competition with China, and in particular in response to its monopoly over processing rare earth metals. Control over investment in strategic sectors has emerged as an effective tool in preventing the outflow of sensitive technology and halting external ownership of strategic infrastructure.

It is significant that the same geo-economic policy is being presented by the European Union, and that further promotes transatlantic cooperation in this area. In 2023, the EU and the USA launched a Joint Transatlantic Forum on Critical Materials, which discusses supply coordination, harmonization of the standards, and collaborative investment projects. This partnership increases the collective resilience of Western economies to external tension and assists in developing an intersocial space of common technology and regulation in the field of extraction, processing and circulation of strategic resources [5].

In addition to measures restricting activity, the USA resorts to economic diplomacy, integrating a mineral component into its regional agenda. Thus, within the Indo-Pacific Economic Framework (IPEF), a block was established specifically aimed at coordinating mineral raw material supplies, simplifying regulatory conditions and activating joint ventures. Dialogue with individual countries – say, with Mongolia, which has significant deposits of rare earth elements – is affected by lending and technical support programs, thereby facilitating the cultivation of dependence on USA aid and technological inventions [6].

Thus, the USA is creating a multi-level model of foreign policy positioning, when economic incentives and limitations are methods of redistributing influence in the sphere of strategic resources. Geoeconomics becomes not just an appendix to foreign policy, but also an integrated part of foreign policy, created to reform international mineral resources access rules.

Innovative technologies and public investment

Emerging technologies and government spending are increasingly the main element of US self-sufficiency in strategic metals. As a result of limited access to raw materials and reliance on external suppliers, the US government has increasingly supported scientific research, modernization of enterprises, and construction of new plants. This process reflects a shift towards a technology-based method of resource protection. It is directed at creating and utilizing new solutions at every phase, ranging from excavation to recycling.

Among the most significant domains is the development of technologies for strategic metals processing in order to reduce foreign capacity dependency. To be more specific, the United States Department of Energy funded the creation of research facilities aimed at the development of new methods for extracting rare earth metals from waste generated by coal mining and recycled materials. ARPA-E and Critical Materials Institute (CMI) programs oversee inter-disciplinary projects aimed at making extraction more efficient and its environmental footprint smaller [7].

A key area is the development of substitute technologies, i.e., new materials that can replace rare metals in critical applications. USA universities and research institutions, including the DOE national labs, are actively engaged in developing equivalent alternatives that can be utilized in electronics, battery systems, and defense applications. At times, these developments are supported by defense programs, including DARPA and DOD. This shows exactly how crucial such technologies are to strategy.

Government funding is also funneled into recycling activities and the establishment of closed-loop supply chains. Initiatives such as those included in the Bipartisan Infrastructure Law, allow for the provision of funds for the establishment of industrial infrastructure along with the development of logistics systems for the recovery of recyclable materials. Early estimates anticipate that during the year 2022 alone, the USA government spent over $1,2 billion on recycling project-related investments and the building of new production plants [8].

Thus, investments in breakthrough technological innovations, along with government support for innovative initiatives, create a long-term basis for minimizing dependency on resources. These strategies enable the USA not only to manage geopolitical uncertainty but also to take a leading role in the emerging framework of the «smart» resource economy.

Conclusion

The analysis reveals that the USA approach to diversifying the supply of strategic metals is complex and has geopolitical, economic, and technological dimensions. As competition for resources intensifies and global instability is on the rise, minimizing critical reliance on imports while advancing national sovereignty in terms of industrial safety has become a fundamental priority. The USA is launching a methodical strategy involving diplomatic coalitions, economic constraints, the encouragement of domestic production, and massive investments in cutting-edge technologies.

The complexity and consistency of these measures point to the formation of a new resource planning model, which gives priority to sustainability, innovative development, and international cooperation with technologically and politically close countries. However, the remaining challenges – environmental constraints, technological barriers, and the slow pace of infrastructure transformation-require further efforts and strategic flexibility.

Библиографический список

1. MINERAL COMMODITY SUMMARIES 2025 / U.S. Geological Survey (USGS) // URL: https://pubs.usgs.gov/periodicals/mcs2025/mcs2025.pdf (date of application: 10.03.2025)2. YTTRIUM / U.S. Geological Survey (USGS) // URL: https://pubs.usgs.gov/periodicals/mcs2025/mcs2025-yttrium.pdf (date of application: 10.03.2025)

3. Joint Statement of the Minerals Security Partnership Principals’ Meeting 2024 / U.S. DEPARTAMENT of STATE // URL: https://2021-2025.state.gov/joint-statement-of-the-minerals-security-partnership-principals-meeting-2024 (date of application: 12.03.2025)

4. Dissanayake E. Build Back Better World vs Belt and Road Initiative: Two Sides of a Political Coin. // NIICE. 2021.

5. Selimov A. Comparative analysis of legal regulation of international transactions in the USA and the EU // International Journal of Scientific Research and Engineering Development. 2024. Vol. 7(6). P. 480-483.

6. Mongolia’s Development of Critical Minerals. Opportunities and Challenges // The National Bureau of Asian Research (NBR). Charles Krusekopf / URL: https://www.nbr.org/publication/mongolias-development-of-critical-minerals-opportunities-and-challenges/ (date of application: 13.03.2025)

7. Smoliarchuk V. Methods and techniques for improving the efficiency of business processes in manufacturing companies // Cold Science. 2025. №13. P. 53-60.

8. Biden-Harris Administration Announces Nearly $74 Million To Advance Domestic Battery Recycling And Reuse, Strengthen Nation’s Battery Supply Chain / U.S. DEPARTAMENT of ENERGY // URL: https://www.energy.gov/articles/biden-harris-administration-announces-nearly-74-million-advance-domestic-battery-recycling (date of application: 13.03.2025)