Introduction

Small and medium-sized enterprises (SME) play an important role in the modern economy, contributing significantly to employment, innovation, and overall economic activity. During age of globalization and the digital economy, this sector faced with some critical challenges like limited financial resource access, transaction costs being high, and improper financial transparency. These problems can limit the potential for business development, preventing its integration into a broader economic context.

In recent years, digital financial tools such as electronic payment systems (EPS), blockchain, crowdfunding, and financial technology (fintech) services have had a significant impact. Their usage encourages the development of more responsive and efficient business models, which affects the sustainability and competitiveness of firms. The goal of this research is to analyze the impact of digital financial tools on the sustainable development of SME.

Main part. Digital financial tools: definition and types

Digital financial instruments are information and communication technology-based products that provide access to financial services, enhancing the efficiency, accessibility, and transparency of financial operations. They include various technologies, platforms, and services that enable the processing, transmission, and storage of digitally formatted information, fundamentally transforming traditional processes.

With the advent of the internet and mobile phones, financial services that previously required physical presence and huge time usage have become available in electronic form. This has created new channels of interaction between clients and institutions, improving access to finance and service quality. One of the most significant digital tools influencing SME growth is EPS. These are payment and money exchange facilitation technologies offered over the internet or other forms of digital channels. They serve as go-between parties in a transaction, effecting secure, fast, and convenient payment in the form of funds transfer and purchase payment for goods and services. Electronic payment is effected across various platforms that include mobile devices, online banking, specialty payment services and payment gateways [1].

One of the most pioneering uses of such platforms by SME is the American company Square, which specializes in providing mobile payment solutions and financial services for small and medium-sized enterprises. Its card reader hardware and mobile apps make it easy for businesspeople to accept payments from debit and credit cards, and mobile wallets. It also offers in-built solutions for inventory management, sales analysis, and tracking financial streams, which actually simplifies business management and makes it more efficient [2].

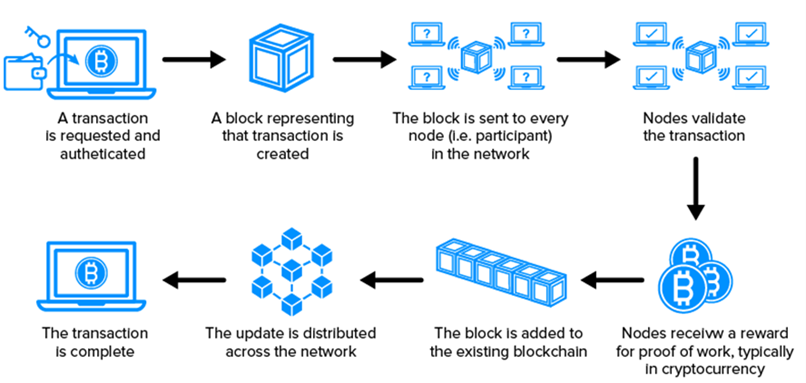

Aside from EPS, blockchain is another important SME tool. It is a distributed data storage and transmission technology based on the principles of decentralization, cryptographic protection and agreement of network participants. Unlike classical centralized systems in which data reside within a point, blockchain has an arrangement in which each transaction is recorded in a series of blocks, with each block having records of the last entry. These blocks are linked with cryptographic methods, so that it cannot be altered by anyone without the consent of all the parties in the network (fig. 1).

Figure 1. The scheme of blockchain technology

One of the popular and successful implementations of blockchain technology among SME is the business Everledger, which uses blockchain to track the origin of commodities, particularly gemstones and diamonds. It creates digital tokens for each gemstone. This allows market participants to trace the history of the stone, its journey through various production and sales stages, and verify its authenticity and freedom from criminal connections. Application of this technology has made the company ensure that it offers top-level transparency to customers as well as increased trust from partners and investors [4].

Another powerful tool to attract capital in the early stage of development is crowdfunding. This is a form of mass financing in which funds for the implementation of a project or startup are collected from private investors on a special online platform. It provides entrepreneurs with the ability to reach out to large groups of people, typically who lack professional investment capabilities.

Crowdfunding is based on several principles that determine its applicability as a method of capital raising. Firstly, there is the principle of masses participating, in that business or project capital is raised from a large community of individual contributors or investors who contribute small amounts. This helps entrepreneurs to access capital without relying on traditional financing sources, such as venture investors or banks. The second core principle is openness and accessibility. Projects launched by crowdfunding platforms are generally publicly displayed, and hence participants and investors may familiarize themselves with the project details and aims. This supports trust in the project and enables prospective investors to make more sound investment choices. Another principle is flexibility and variety of funding models. Crowdfunding offers several forms of engagement, including donations, pre-orders, equity participation, and lending. Depending on the model employed, investors receive rewards, company ownership, or even financial returns in the future. Additionally, community support and social proof play a significant role. Whether a campaign succeeds or fails typically depends on how aggressively it is shared by contributors and how the project is perceived by the community.

Two of the popular crowdfunding sites in the U.S., providing SME a unique opportunity to raise money for the completion of their projects, are Kickstarter and Indiegogo [5]. The first is devoted to creative and innovative ventures, offering entrepreneurs the opportunity to fundraise for innovative products and services, even such sectors as technology and ecology. On the other hand, Indiegogo is less stringent with funding terms and provides a fixed and flexible option, which is accommodative for startups at different stages of growth. Both platforms supplement each other in enhancing SME access to capital through providing entrepreneurs with alternative channels to access funds and get a backing customer base.

Another cutting-edge product developed on the basis of the use of digital technologies to improve and maximize financial services is fintech services. They are an excellent range of instruments facilitating easier provision and receipt of services, increased accessibility, and reduced costs. They can be conditionally subdivided into several types depending on their function (table 1).

Table 1

Types of fintech services [6, 7]

| Type of fintech service | Description | Examples of services |

| Online lending | Platforms for providing loans to SME via the Internet, bypassing traditional banks. | LendingClub, Funding Circle, Prosper |

| Financial management | Tools for income and expense accounting, budget planning, and tax liability optimization. | QuickBooks, Xero, Wave |

| Payment services | Services that allow SME to accept payments, manage financial transactions, and analyze revenue. | Square, PayPal, Stripe |

| Investment and asset management | Platforms for investment, analysis, and asset management, often with elements of automation and algorithmic solutions. | Robinhood, Wealthfront, Acorns |

| Digital banks | Digital platforms that provide a full range of banking services, including checking accounts, loans, and transfers without the need for physical branches. | Chime, Varo, Ally |

These services, according to the author, are a set of solutions that have an important role in making the financial sector modern. They introduce access to tools to SME which were either not available previously or required much time and effort.

Thus, these financial digital solutions offer accessibility, security, and convenience, significantly improving the business environment. Technologies continue to evolve, delivering new instruments and opportunities for more effective interaction with financial markets, making them an integral part of the sustainable development of businesses in the context of the digital economy.

Advantages of using digital financial tools in the development of SME

Financial digital means are increasingly shaping the sustainable SME development, presenting entrepreneurs with new opportunities to organize processes and render them more effective. The greatest advantage of introducing them is surely the reduction of transaction costs. Physical financial systems involve many middlemen, such as payment systems, banks, and financial institutions, which necessarily incur additional costs, like transfer fees, currency conversion, and payment processing and administrative fees. Digital financial tools, however, minimize the number of middlemen, resulting in a radical reduction of operational costs related to finance.

For example, EPS enable the transfer and payment of goods and services instantly without the physical presence of the parties, which significantly reduces time and cost of transactions. Blockchain, with its decentralized structure and cryptography, eliminates the need for intermediaries, resulting in lower costs for intermediary services and additional savings on transactions. For small businesses, where even small amounts are important, significant cost savings can be a significant factor in financial stability and growth.

Apart from that, the financial digitalization opens opportunities for SME to raise capital more widely. Traditional capital-raising tools, such as bank credit, may not be accessible to these enterprises under certain conditions due to stringent requirements, high interest rates, or the lack of suitable guarantees [8]. On the other hand, digital financial instruments, such as crowdfunding and fintech services, generate new ways for raising capital.

Financial digitalization also gives rise to higher financial transparency, required in order to create higher levels of trust from the side of investors, partners, and clients. Traditional financial systems attempt to limit the delivery of information regarding transactions, and it is difficult to trace the money flow and therefore can create potential risks for third-party players. On the other hand, blockchain technology, for example, ensures transparency of all financial transactions by recording every transaction in an immutable public ledger that can be seen by all users of the network. This not only reduces the possibility of fraud and errors but also facilitates greater trust between companies and their customers or investors.

For SME, which have difficulty in obtaining external funding, high transparency of operations is a precious asset for competition. Investors know that all operations can be easily checked, so they are more likely to invest in highly financially transparent companies. Accounting financial operations on digital platforms and communicating with clients on digital platforms also allow entrepreneurs to exercise better control over their cash flows and minimize risks. This level of transparency not only enhances the level of trust among the external partners but also strengthens the internal stability of the firm, as the business becomes predictable and more manageable.

Conclusion

Incorporation of electronic financial instruments into SME operations opens up new visions for its growth and sustainability. These innovations reduce transactions costs significantly, make more capital available, and ensure high financial transparency. Fintech services, EPS, crowdfunding and blockchain open opportunities for entrepreneurs to make the most of financial transactions and simplify fundraising process and asset management. Digitalization of these processes not only reduces costs, but also contributes to the creation of more flexible and competitive business models.

Библиографический список

1. Nurdinova K. Integration of Artificial Intelligence Into Accounting as a Tool for Optimization and Risk Management // Bulletin of Science and Practice. 2024. Vol. 10. № 12. P. 405-410. DOI: 10.33619/2414-2948/109/52 EDN: KMHNQI2. Electronic Payment Systems – What You Need to Know / Square // URL: https://squareup.com/gb/en/the-bottom-line/managing-your-finances/electronic-payment-systems (date of application: 20.02.2025)

3. Ponomarev E.V. The role of technological innovations in enhancing consumer protection in the financial sector // Dnevnik nauki. 2024. № 6. [Electronic resource]. URL: http://www.dnevniknauki.ru/images/publications/2024/6/technics/Ponomarev.pdf EDN: NVGWQM

4. Shaikh A. R., Ali I. Driving Business //Handbook of Digital Innovation, Transformation, and Sustainable Development in a Post-Pandemic Era. 2024. Р. 34.

5. Chen W. D. Crowdfunding: different types of legitimacy //Small Business Economics. 2023. Vol. 60. №. 1. Р. 245-263. DOI: 10.1007/s11187-022-00647-0 EDN: DJBRPE

6. Balgimbayev A. The evolution of digital payments in the global economy: the role of fintech startups and national initiatives // Cold Science. 2024. № 12. P. 38-47.

7. Łasak P. The role of financial technology and entrepreneurial finance practices in funding small and medium-sized enterprises //Journal of Entrepreneurship, Management and Innovation. 2022. Vol. 18. №. 1. Р. 7-34. DOI: 10.7341/20221811 EDN: YEOLXL

8. Li W., Pang W. Digital inclusive finance, financial mismatch, and the innovation capacity of small and medium-sized enterprises: Evidence from Chinese listed companies //Heliyon. 2023. Vol. 9. №. 2. DOI: 10.1016/j.heliyon.2023.e13792 EDN: YKCERJ